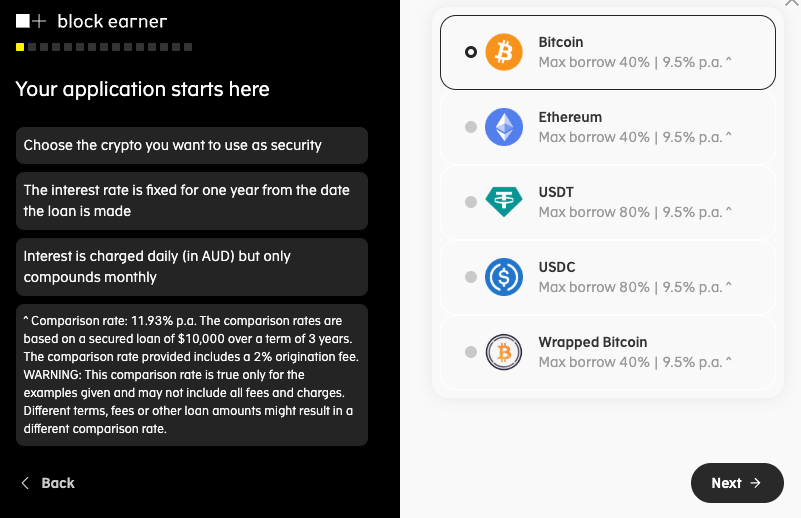

Loan options for end users are referred to as loan offers. These offers define the types of loans users can apply for and the rules governing these loans, such as the security currency and the maximum LVR (Loan-to-Value Ratio).

Key Concept for Loan Offers

- Loan Ratio: The maximum LVR an end user can borrow when opening a new loan or performing a redraw.

- Origination Fee: A one-time fee charged at the initiation of a loan, calculated based on the loan amount, and added to the loan balance. This fee supports loan processing and setup. The same fee applies to redraws.

- Loan type: There are two types of loans:

- Fixed Term: A loan with a set duration and fixed repayment schedule.

- Line of Credit: A flexible loan where users can draw funds up to a pre-approved limit.

- Automatic Repayment: This feature defines how repayments are triggered when the LVR exceeds predefined thresholds:

- Automatic Repayment Threshold: The LVR level that triggers an automatic repayment.

- Automatic Repayment Target: The LVR level to which the repayment will reduce the balance after being triggered.

- Automatic Repayment Method:

- Manual: When set to manual, the repayment is not automatically executed. A default notice is sent to the user, who is required to reduce their LVR to the

Automatic Repayment Targetwithin 30 days. If the user fails to do so, a manual repayment will be executed on their behalf to bring the LVR back to the target level. - Automatic: Repayment is automatically triggered when the LVR reaches the Automatic Repayment Threshold.

- Manual: When set to manual, the repayment is not automatically executed. A default notice is sent to the user, who is required to reduce their LVR to the

Difference between Fixed Term and Line of Credit

The main difference between a Fixed Term Loan and a Line of Credit lies in the loan duration and the monthly repayment requirements.

| Line of Credit | Fixed Term | |

|---|---|---|

| Loan duration | 12 months | 3-5 years |

| Monthly repayment | No requirement | Require monthly repayment |

| Loan application | No payslip required | A payslip or proof of income required |

How does the loan offer apply to the customer

One Loan Offer per Asset and Loan Type:

Each user is limited to one loan offer per asset type and loan duration. For example:

- A user can have one BTC Line of Credit Loan offer.

- A user can also have one BTC Fixed Term Loan offer.

- The same structure applies to other assets like ETH, USDC, etc.

Default Loan Offers

Block Earner sets up default loan offers to ensure consistency and ease of integration, defining the baseline terms for loans. These default offers are tailored to user types, with personalized options for individuals and specialized configurations for businesses and organizations.

Example

For a personal user holding BTC:

- Loan Offer 1: BTC Line of Credit Loan (e.g., 12-month term with up to 40% LVR for flexible use).

- Loan Offer 2: BTC Fixed Term Loan (e.g., 3-5 year term with a fixed interest rate and up to 50% LVR).

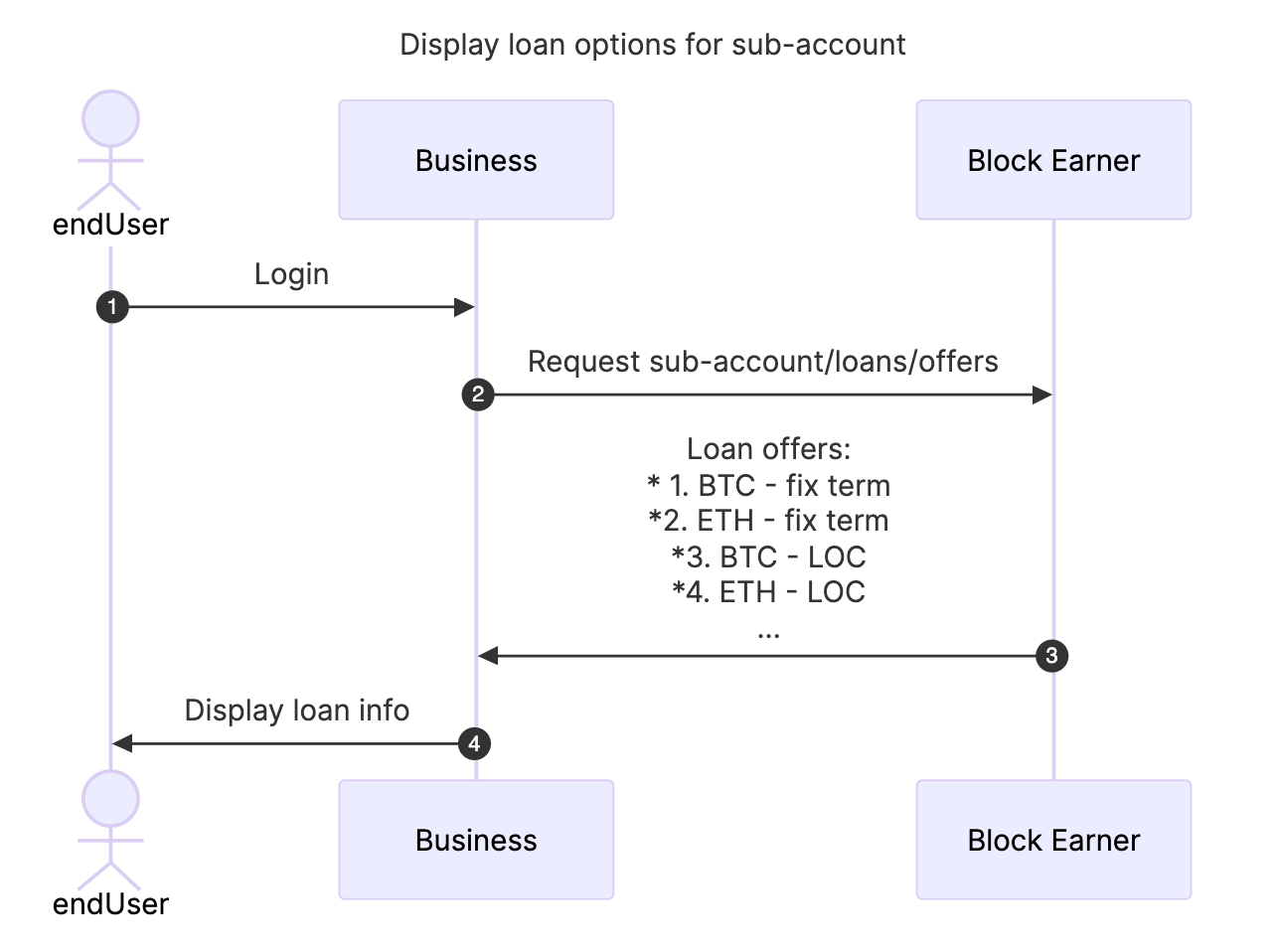

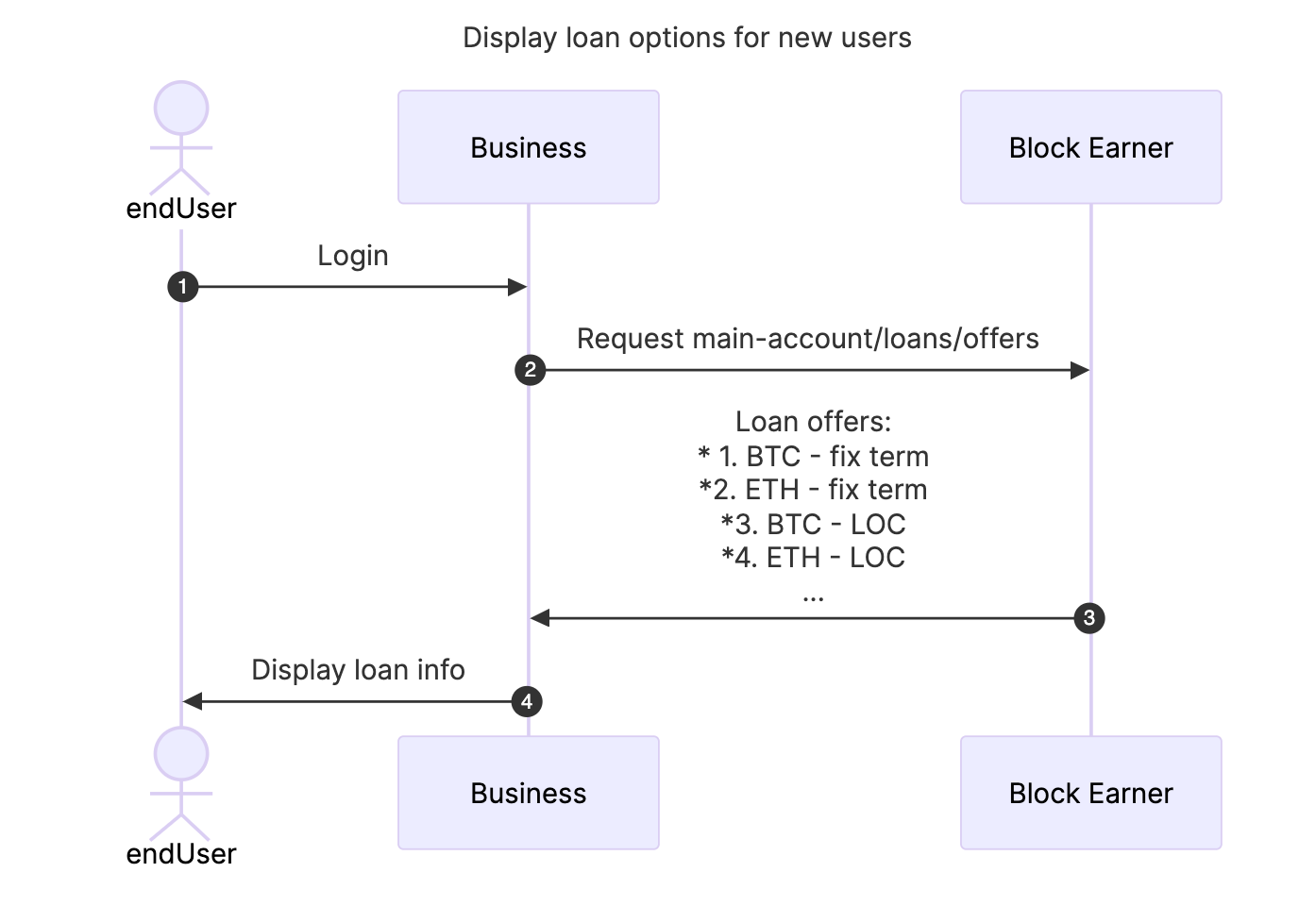

API for displaying loan offers

Before sub-account creation, use Get loan offers for main account API to request the loan offers for main account

After sub-account creation, use Get loan offers for sub-account API to request the loan offers for the sub-account. Block Earner recommends to create a sub-account for an end-user when the user first shows interest to the loan application, or when you'd like to setup a bespoke loan offer for a customer.

Note:

The default loan offers are same for both main account and sub-account. However the sub-account always holds the most accurate offer for a specific end user therefore it's recommended to use the sub-account offer as much as possible.

Display loan offers for new user (no sub-account creation)

Display loan offers for sub-account user